Retirement

If you are approaching retirement, or already there, you face an increasingly complex challenge – making your money last throughout your lifetime.

In retirement you will have to rely on your savings to cover your expenses, whether those savings come from a government plan, employer plan or money you have saved on your own. If your assets are not wisely placed or if you draw too much money, those mistakes can be very difficult to fix. There are Five Key risks to achieving a secure income for life:

At TRP Retirement Planning we can help you develop a formal, written plan for building up retirement assets and drawing down retirement income in a manner likely to last you your lifetime.

If you already have a financial plan, bring it out, rethink it, and then revise it as needed to incorporate your understanding of the risk factors above. Here are some other things to think about:

- Envision the retirement lifestyle you want

- Identify your retirement expenses and analyze which are essential and which are discretionary

- Review the income, accounts and other assets available to fund your retirement.

- Compare expenses to income. Earmark known or predictable assets to cover essential expenses, and assign less-predictable assets to fund discretionary expenses.

- Allocate your portfolio appropriately for your timeframe, your willingness to take risk, and your overall financial situation

- Ensure your portfolio is set up to help minimize any foreseeable or likely risks.

- Monitor your plan regularly, at least bi-annually, with your advisor. An out of date or unrealistic plan is not of practical use in helping you achieve income to last throughout your lifetime.

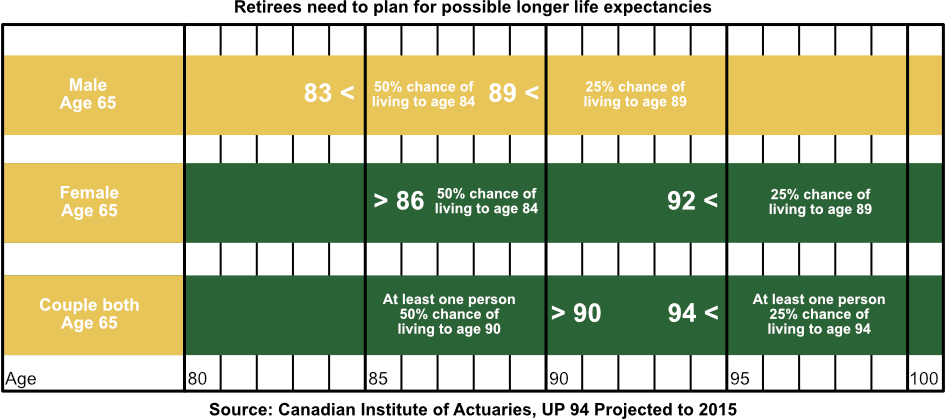

Longevity

A successful retirement income plan helps you ensure that your assets will last throughout your lifetime. Based on today’s higher average life expectancies, plus the possibility that an individual may live well past the average, investors need to plan for 30, 40 or even more years of retirement. If not you run the risk of outliving your savings.

Challenge:

Many people under-estimate how long they could live. As a result, they risk outliving their assets.

what you can do:

When setting up your retirement income plan, allow for the possibility that you’ll live longer than you expect.

Inflation

Inflation is the long-term tendency of money to lose purchasing power. It impacts retirement income planning in two ways.

- Increase the future costs of goods and services

- Potentially erodes the value of assets set aside to meet those costs.

Don’t let the low rates of inflation fool you; even in the 1900’s overall cost rose more than 20%. In the last half of the 20th century, inflation eroded Canadian’s purchasing power by 90% – reducing a 1950 dollar to the equivalent of about 10 cents today.

In other words, inflation is the norm and not the exception. As your costs go up the value of your savings go down.

Even low inflation of rate 2% can have a significant impact on your savings and its purchasing power. If you started with an income of $46,000 per year, 25 years later it would it would only be approximately $28,000 per year, a decline in purchasing power of 39%.

Challenge:

Inflation increases future costs of goods and services and erodes the value of assets set aside to meet those costs.

What you can do:

Include investments with the potential to outpace inflation in your long-term portfolio.

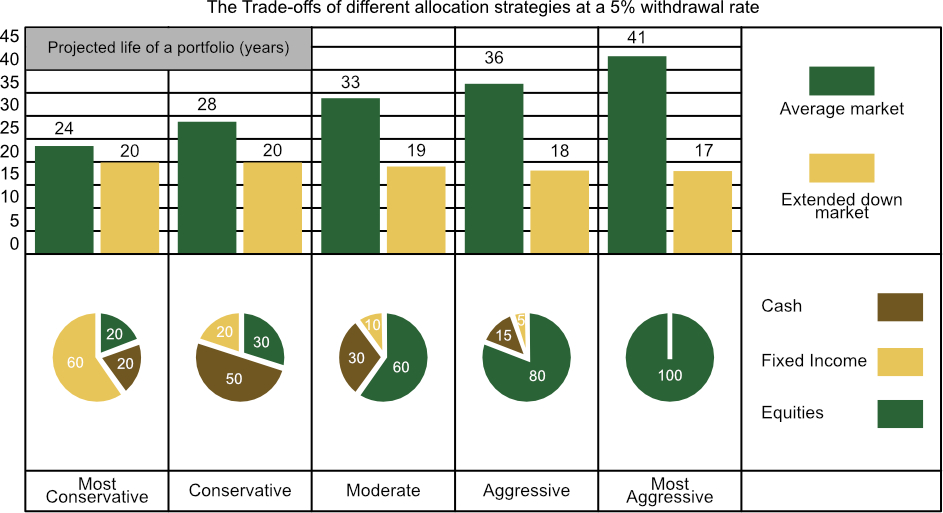

Asset Allocation

“The market goes up, the market goes down.” This adage is as true today as it was at any time in history. And while this adage is true, it is also true that equity assets (Stocks or Equity Mutual Funds) have tended to produce higher long-term returns than fixed-income investments such as Fixed Income or GIC’s. That is why people saving for retirement are generally advised to put a portion of their retirement savings into equity investments.

Even in retirement, you’ll probably do best with a portfolio where your assets are allocated to a variety of different investment types and styles. You will want neither all equities, which can be volatile, nor all fixed income, which may mitigate some downside risk but may not produce the growth that you need.

The graph above depicts how long a portfolio is likely to last at a 5% inflation-adjusted annual withdrawal rate, given 5 different asset allocation strategies. It projects how long a portfolio will last under two different market conditions, an average market and a prolonged market decline.

As you can see the most aggressive portfolio, composed of 100% equities may only last 17 yours in a prolonged market downturn, versus 20 years for a conservative portfolio. However, the conservative portfolio may not allow enough growth to last a lifetime. Under average conditions the conservative portfolio may only last 28 years versus 41 years for the most aggressive portfolio.

Challenge:

Retirees need investments they can rely on to produce regular income. But these ‘safe’ investments may not grow enough to keep up with inflation and provide income over the long term.

What you can do:

Even in retirement, your best strategy may be to build a balanced portfolio that combines equities with Fixed Income and cash investments (GIC’s, money markets). The exact mix will depend on your individual circumstances.

Excess Withdrawal

How much you withdraw or spend form your savings on a regular basis will dramatically affect how long those savings will last. The rate of withdrawal you select can significantly shorten or lengthen the life of your assets. Until recently, many people in the early years of retirement assumed they could afford to withdraw 7%, 8% or more per year because of high equity returns. In fact, a more conservative inflation-adjusted withdrawal rate appears to be more sustainable.

Cutting back your discretionary living expenses, taking on part-time work, or investing strategies that will provide greater growth for your assets are all possible ways to minimize the amount you need to withdraw from your savings. You may be better off if you withdraw as little as possible in your early retirements years, then if your portfolio does well, you can withdraw more latter on, when there is less risk you will run out of money.

Challenge:

Withdrawal rates over 4 – 5% begin to increase the likelihood that you will run out of savings.

What you can do:

Use a conservative withdrawal rate, particularly in the early years of retirement.

Health Care Expenses

Even though Canada has one of the best health care systems in the world some of the items or services you may need or want in the future may not be included.

For example, close to half of retirees now turning age 65 will be admitted to long-term care facilities at some point in their lives. Nearly 25% will stay there one year or more, and about 10% will stay 5 years or more. Since the government only pays a small portion of these costs, this can be a major expense. Other health care expenses that are covered only partially, or not at all include nursing care at home, private or semi-private hospital rooms, or home renovations to deal with disabilities.

In the meantime there are serious concerns about the rising costs of healthcare in Canada. At the present time no one is sure how the issue will be resolved. You should be prepared that, in the future, individual Canadians may pay more of their health care costs.

Challenge:

While our national health care system provides coverage for basic medical needs, it does not cover everything. Individuals may need or want additional items and services. There is also some concern that individuals may have to bear more of the health care expenses in the future.

What you can do:

While health care expenses in retirement are hard to determine, they should be included in retirement planning. Extra savings and/or insurance may give you more choice in the future as well as peace of mind.